‘GPF Withdrawal Rules’ PDF Quick download link is given at the bottom of this article. You can see the PDF demo, size of the PDF, page numbers, and direct download Free PDF of ‘GPF Withdrawal Rules’ using the download button.

General Provident Fund Withdrawal Rules PDF Free Download

GPF Rules PDF

What is GPF?

In the General Provident Fund, the government employees contribute a small part of their salaries to the GPF account. They can get their accumulated funds at the time of retirement (maturity date).

It is mandatory for the GPF subscribed employees to contribute their monthly share regularly unless there is a case of suspension. However, employees 3 months close to retirement can stop contributing.

What are the GPF Rules?

When it comes to the General Provident Fund rules, there can be several classifications based on each aspect or feature of this savings instrument. These are –

Eligibility Rules

One of the primary sets of rules is concerning this PF’s eligibility. These are listed in the pointers below –

- Any permanent government employee who is an Indian resident can subscribe to GPF.

- All temporary government employees with an employment record of 1 year or more are eligible for GPF.

- Government employees working in organisations functional under the EPF Act, 1952 can also reap this PF’s benefits.

- Any retired government pensioner who has been re-employed and is not eligible for the Contributory Provident Fund can also subscribe to GPF.

As per GPF rules, it is exclusive to government employees. This is unlike other PFs, which are open to individuals employed in the private sector as well.

Deposit Rules

As is characteristic of other PFs, the General Provident Fund also features set stipulations on the deposit amount and frequency. These have been discussed in the table below.

| Minimum amount | The amount that a subscriber contributes shall not be less than 6% of his/her total income. |

| Maximum amount | A subscriber cannot contribute any amount that exceeds his/her total income. |

| Frequency | Individuals shall make a deposit every month. But, it does not apply when such a subscriber is suspended. |

| Maturity date | The PF matures at the date of one’s retirement or superannuation. However, contributions continue until 3 months before retirement as per GPF rules. |

Nomination Rules

Individuals can declare a nominee when first subscribing to the General Provident Fund. As per rules, the nominee should be a family member.

Subscribers may also declare more than one nominee. In that case, he/she should also specify the share of each nominated entity. It is also possible to appoint a minor when he/she reaches the majority age, i.e. 18 years.

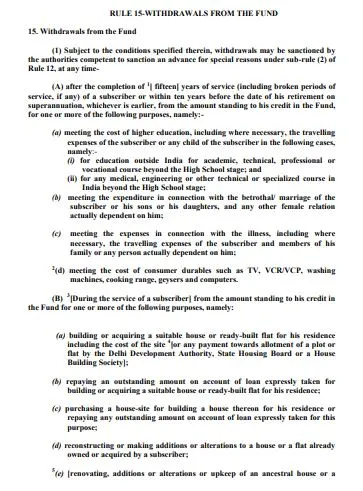

Withdrawal Rules

Perhaps the most pertinent of all is the GPF withdrawal rules. The primary criterion here is that individuals must complete at least 10 years of service before being eligible to withdraw from their GPF. Prior to 2017, this limit was set at 15 years.

The following points discuss the rules surrounding withdrawal from a General Provident Fund account –

- A subscriber can withdraw an amount equal to 75% of the outstanding balance in such PF or his/her 12 months’ emoluments, whichever is lower. It is available for purposes of funding education or any ceremony, such as the marriage of self or a dependant family member.

- Individuals can withdraw up to 90% of the outstanding balance in case of illness of self or a dependent family member. According to new GPF withdrawal rules, the amount can be availed within 7 days for such purposes.

- Subscribers can finance purchasing a house, buying land for the construction of a house, repaying an existing home loan, reconstruction or renovation of home, or repairing the ancestral house, by means of GPF withdrawal. The amount is capped at 75% of the outstanding balance in the General PF.

- Withdrawal may also be made to buy a vehicle, make a deposit for purchasing a vehicle, repay a car loan, or repair a vehicle. If it’s for purchasing a vehicle, the maximum amount that one can avail is 75% of the balance or three-fourths of the cost of such a vehicle, whichever is lower.

- Individuals may choose to withdraw 90% of the balance amount in their GPF without providing any cause prior to 2 years from retirement. This privilege was earlier reserved 1 year before retirement.

According to GPF rules, individuals can also withdraw from their accounts to purchase consumer durables, like a washing machine, air conditioner, etc. Nonetheless, it is necessary to utilise the withdrawn amount only for the stated purpose.

Aside from premature withdrawals, the outstanding amount can also be released in the event of a subscriber’s death. The nominee is also entitled to an additional amount, which is equal to the average of three years of PF balance preceding such event. However, such an additional amount cannot exceed Rs.60,000.

As per GPF part final withdrawal rules, the subscriber should have been in service for 5 years or more for such additional benefits.

Apart from these, subscribers are entitled to the full amount upon retirement or superannuation.

GPF Interest Rate Rules

The GPF balance earns interest throughout. The Central Government revises such rate from time to time. For the recent quarter, this rate had been set at 7.1%.

Taxation Rules

The General Provident Fund is one of the most lucrative savings instruments for its tax benefits. The contributions made, interest accrued, and returns received are tax-exempt under Section 80C of the ITA, 1961.

| Language | English |

| No. of Pages | 64 |

| PDF Size | 0.1 MB |

| Category | Government |

| Source/Credits | pensionersportal.gov.in |

General Provident Fund Withdrawal Rules PDF Free Download