‘NCERT Solutions for Class 11 Accountancy Chapter 14 Structuring Database for Accounting’ PDF Quick download link is given at the bottom of this article. You can see the PDF demo, size of the PDF, page numbers, and direct download Free PDF of ‘Ncert Class 11 Accountancy Chapter 14 Exercise Solution’ using the download button.

Structuring Database for Accounting System NCERT Textbook With Solution PDF Free Download

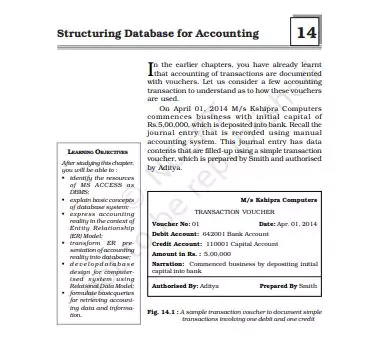

Chapter 14: Structuring Database for Accounting System

The process of computerised accounting involves identifying, storing and retrieving the data content of an accounting transaction.

This requires a mechanism to store such data content of vouchers in a manner that allows its easy and convenient retrieval as and when required.

This is achieved by designing suitable database for accounting. Such a database consists of inter-related data tables that are structured in a manner that ensures data consistency and integrity.

In this chapter we shall discuss the basic concepts of database system of accounting.

Data Processing Cycle In order to understand the dynamics of database design, let us understand the data processing cycle in the context of accounting.

Data processing involves the technique of collecting, sorting, relating, interpreting and computing data items in such a manner as to provide meaningful and useful information for decisionmaking.

The necessary steps involved in data processing cycle are data capturing, inputing, processing and generating information available to the user Both computerised and computer-based AIS require a definite data structure for storing the accounting data.

As already mentioned, the databases are used for storing accounting data. The process of designing database (for accounting) begins with a reality (or accounting reality) that is expressed using elements of a conceptual data model.

The process of designing a database for accounting is best described through a flow chart (Figure : 14.4). Reality : It refers to some aspect of real world situation, for which database is to be designed.

In the context of accounting, it is accounting reality that is to be expressed with complete description. ER Design : This is a formal blue print, with a pictorial presentation, in which Entity Relationship (ER) Model concepts are used to represent description of reality. Relational Data Model :

It is representational data model through which ER design is transformed into inter-related data tables along with the restriction in the form of rules that are specified to ensure the consistency and integrity of stored data.

It is a popular conceptual data model, which is mostly used in database-oriented applications.

The major elements of ER Model are entities, attributes, identifiers and relationships that are used to express a reality for which a database is to be designed.

The model is best depicted with the help of ER symbols, the list and description of which is shown in figure 14.5.

While preparing an ER Diagram, the following symbols are used to represent different types of entities, attributes, identifiers and relationships :

Anything in the real world with independent existence is called entity such as an object with physical existence (e.g. car, person, house) or conceptual existence (e.g. a company, job, university course, account, voucher).

In the context of above accounting reality, there exist five entities: Accounts, Vouchers, Employees, AccountsType and SupportDocuments.

The accounting data is captured through these entities Attributes are some properties of interest (or characteristics) that further describe the entity such as height, weight and date of birth in case of a person and code and name in case of accounts.

An entity has a value for each of its attributes, which is the data stored in the database.

There are several types of attributes of an entity that have been described as follows : (i) Composite vs. Simple (or atomic) attributes : The composite attributes can be divided into smaller sub-parts to represent some more basic.

| Author | NCERT |

| Language | English |

| No. of Pages | 50 |

| PDF Size | 0.5 MB |

| Category | Accountancy |

| Source/Credits | ncert.nic.in |

NCERT Solutions Class 11 Accountancy Chapter 14 Structuring Database for Accounting System

1. State main categories of data models.

Ans: Any information system’s primary function is to manage enormous amounts of structured and unstructured data. Data models explain how data should be stored in data management systems such as relational databases, including the structure and integration features.

The most frequent types of data models are: hierarchical database model, relational database model, network model.

i. Relational Data Model- This data model is based on the relationship between the values of the collected data. Data is organized into rows and columns in this data model. A tuple is a row, a column header is an attribute, and the entire set of rows and columns, i.e. a table, is referred to as a relation. Because it expresses the relationship between the rows and columns, the table is referred to as a relation. This model describes the data structure and provides storage and retrieval functions.

ii. Hierarchical Data Model- Records and parent-child connections are the key components of the hierarchical data model.

A record, on the other hand, is a collection of values that gives information on an entity or a relationship, whereas a parent-child relationship illustrates the relationship between the parent and children record types. Instead of an arbitrary graph, the records in this data model are organized in a tree structure.

iii. Network Data Model- The initial network model was published in CODASYL DataBase Task Group’s 1971, which is why this form of the data model is also referred to as the DBTG model (DBTG).

This data model is made up primarily of records and sets. While data is kept in records, which are collections of linked data values, sets represent the relationship between two types of records.

2. How are computers useful in processing the accounting data?

Ans: For most firms, the manual system of accounting has traditionally been the most prevalent way of keeping records of financial transactions/accounts.

An accountant used to keep the books of accounts in the old days on a daily basis, such as cash books, accounting diaries, and ledgers on a regular basis, and it’s utilized to put together a transaction summary and a final report on a manual basis.

The complexity of transactions increased exponentially as speed, storage, and processing capacity increased. It became critical to keep accounting data up to date in real-time (or on the spur of the moment). As a result, computerized accounting systems have become more convenient and quick.

The features listed below are provided by a computerized accounting system:

- Accounting data is entered and stored online; purchase receipts and sales invoices are printed; and each account and transaction entry is unique.

- Account grouping can be done right from the start.

- Instant management reports at the touch of a button

In the end, computers have proven indispensable in today’s accounting departments.

Related PDFs

Fundamental Of Accounting And Tally Prime Notes PDF

NCERT Class 11 Accountancy Textbook Chapter 14 Structuring Database for Accounting System With Answer PDF Free Download